News

AutoWallis closed the first quarter with improving efficiency

2026.05.21.

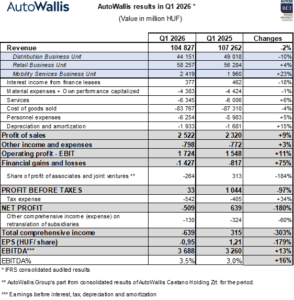

The AutoWallis Group improved its operating efficiency in the first quarter of 2026, as EBITDA increased by 13% to HUF 3.7 billion, primarily due to an improvement in gross margin. The favorable development was achieved despite a 2% decline in revenue, caused by a decrease in wholesale sales volumes, in contrast to growth in the Retail and Mobility Services Business Units.

The Group’s profitability for the period was adversely affected by several one-off factors, including non-recurring costs related to the introduction of new brands in line with its growth strategy, as well as partly unrealized financial losses resulting from the strengthening of the Hungarian forint.

The AutoWallis Group further improved its operating efficiency in the first quarter of 2026, while its revenue of HUF 104.8 billion remained essentially unchanged (-2%) compared to the same period of 2025. The slight decline occurred alongside a temporary 10% decrease in the revenue of the Distribution Business Unit, while the Retail Business Unit expanded by 4% and the Mobility Services Business Unit by 23%. Thanks to acquisitions and developments completed in previous years, the Company’s international position remains strong, with 63% of revenue generated from foreign markets. The number of new passenger car registrations in the EU increased by 4%, while in the Group’s region – with the exception of Slovakia (-2%) and Romania (-19%) – growth exceeding 5% on average was recorded in the first quarter of this year compared to the same period of the previous year. The improving operating efficiency of the AutoWallis Group is reflected in the fact that EBITDA increased by 13% to HUF 3.7 billion in the first quarter of 2026, while the EBITDA margin improved from 3% to 3.5%. The improvement in operating efficiency was primarily driven by higher gross margins, as well as efficiency improvement measures introduced last year largely in response to rapid growth, alongside cyclical market trends. It also had a favorable impact that the Group’s cost base remained broadly unchanged in the first three months of the year. At the same time, the Company reported a total comprehensive income of negative HUF 640 million, while earnings per share amounted to HUF -0.95. The decline is mainly attributable to the initial costs of newly launched brands, dealerships and business developments, which place a disproportionate burden on the start-up period, as well as to foreign exchange losses – partly unrealized – resulting from unfavorable exchange rate developments. Results were also adversely affected by the HUF 264 million loss attributable to AutoWallis from companies jointly managed with strategic partners, in which it holds a 50% ownership stake, compared to a profit of HUF 313 million in the same period last year. In the case of these activities as well, the decline is explained by costs related to the ramp-up of business developments, as well as the significant downturn in the Romanian automotive market. The developments and the introduction of new brands represent strategic investments that establish the foundations for further growth and value creation, while temporarily weighing on the Group’s profitability in the short term.

At AutoWallis, listed on the Prime Market of the Budapest Stock Exchange, cost of goods sold (COGS) declined by 4% to HUF 83.8 billion, a greater decrease than the decline in revenue, while gross margin generating capacity improved from 18.6% to 20.1%. Personnel expenses increased by 5% to HUF 6.3 billion, primarily due to the opening of the Debrecen dealership in the fourth quarter of 2025, as well as wage increases implemented in response to labor market changes (the Group’s average headcount at fully consolidated companies increased by 4% to 1,479 employees in the first quarter compared to the same period of 2025). The negative balance of financial income and expenses deteriorated by HUF 610 million in the first quarter of 2026 compared to the same period of the previous year, reaching HUF -1.4 billion overall (+75%). The balance of interest expenses and interest income remained at the same level as in the comparative period; the increase in financial expenses related to leases is attributable to the larger fleet size in the Mobility Services Business Unit, as well as newly leased properties.

Of the three business units of the AutoWallis Group, the Mobility Services Business Unit delivered the strongest growth in the first three months of the year: its revenue increased by 23% to HUF 2.4 billion, driven by the stronger performance of car-sharing and rent-a-car services, fleet growth in long-term rentals (+5.4%), and the expanding customer base. The Retail Business Unit also expanded, with revenue increasing by 4% to HUF 58.3 billion, alongside a 7% increase in new vehicle sales and a slight 1.4% decrease in used vehicle sales (the latter due to a strong base effect). In the domestic market, AutoWallis’ Retail Business Unit sold 6% more vehicles, while thanks to its diversified country portfolio, sales increased by 24% in Slovenia and by 13% in the Czech Republic. Revenue growth in the business unit was partly attributable to the opening of the Debrecen dealership in the fourth quarter of 2025, and partly to organically increasing sales volumes. The fact that revenue growth was lower than the increase in unit sales is explained partly by product mix effects and partly by the higher level of intra-group sales compared to the previous period. Revenue in the Distribution Business Unit declined by 10% to HUF 44.2 billion in the first quarter of the year, primarily due to a 5.8% decrease in vehicle sales volumes. The contraction was mainly attributable to the decline in KGM sales (-1,066 units). Traditional brands were adversely affected by price competition driven by Chinese brands, to which KGM responded with repositioning, the positive effects of which management expects to materialize from the second quarter onward. The decline in Dacia sales observed across Europe is temporary and mainly attributable to logistics and production factors as well as the transformation of the model range. At the same time, Opel’s performance continued to improve (+519 units), and Nissan sales operations launched in Romania last year also showed growth (+498 units). As a result of these factors, the decline in the Distribution Business Unit is considered temporary.

Commenting on the first-quarter results, Gábor Ormosy, CEO of the AutoWallis Group, said that the slowdown and decline in revenue and profitability were primarily attributable to one-off effects. He highlighted that despite increasing competition, the Company significantly improved its operating efficiency, partly thanks to an 8% increase in gross sales margins and partly due to the efficiency improvement measures introduced last year, largely in response to rapid growth. The developments implemented by the Company in 2025, the opening of new dealerships, and the addition of new brands to the portfolio may increasingly contribute first to revenue growth and then to profit growth in the coming periods. The strategic targets set previously remain achievable, and the results provide a stable foundation for the continuation of the growth strategy.

AutoWallis investor presentation 2026Q1

AutoWallis_reporting-tables_26Q1

Latest news

Extraordinary information – principal and interest payment

2026.07.27.

Extraordinary information regarding a transaction by a person discharging managerial responsibilities

2026.07.15.

Sales Report H1 2026: New vehicle sales continue to accelerate in AutoWallis’ Retail Business Unit

2026.07.15.

Extraordinary information

2026.07.14.

Number of voting rights, composition of share capital 30.06.2026

2026.06.30.